There are many models that facilitate group practices, the most common being a service trust model.

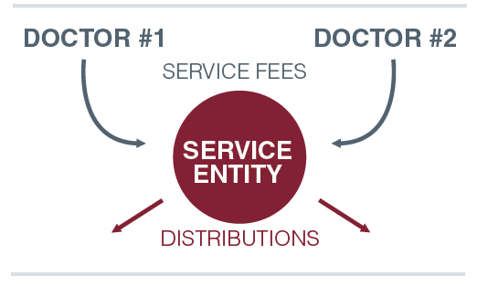

Let’s start with the most simple model - two doctors. Both contribute to the costs of running the practice, either on a set fee per month or a set percentage of gross billings.

Both pay this amount into a service trust which then pays for all administrative and some medical expenses. Hopefully, with good management there is a profit after contributions (service fees).

Sounds simple enough?

Well, consider the situation above where one doctor’s medical fees are much larger than the others and both are paying the same percentage service fee. Now there’s an imbalance in the contribution to profit in the service trust to the detriment of the higher earning doctor.

Our previously simple distribution model has become more complicated and this is where open communication and understanding of your corporate structure becomes very important.

Another variation of this scenario is where both doctors may own the service trust equally but one doctor only works three days per week from the surgery. In this situation, contribution on a flat rate may not seem fair to the part-time doctor.

However, contribution based on a percentage of fees may not be fair to the other doctor as there is a minimum cost involved in keeping the practice running.

These issues are very common and we have seen at first hand the damage they can do to the smooth running of the practice and, on occasion, to personal relationships.

To overcome these profit sharing issues, we recommend the utilisation of a Unit Holders or Shareholders Agreement.

Some key points covered in such an agreement are:

• Minimum level of service fee commitments.

• Details of how service fees are calculated.

• The amount of Annual Leave/Absence allowed from the practice.

• Details of when you can or must exit the practice.

• Details of how profits will be distributed.

• Details of how much your interest will be worth on exiting.

• Details of how you can deal with your ownership interests, who you can sell to, who can buy.

With the key issues clearly articulated, expectations can be openly communicated and managed up front, avoiding the potential for problems further down the track.

So while the discussion may be delicate, it’s one well worth having.