Pre-Open Data

Key Data for the Week

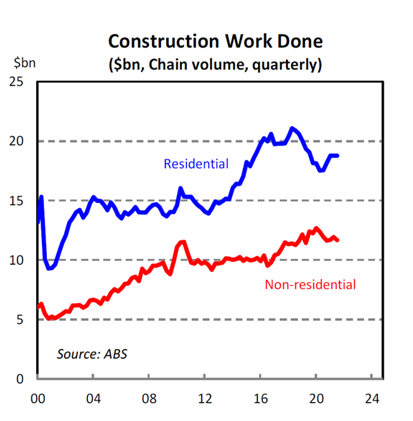

- Wednesday – AUS – Construction Work Done was down just 0.3% in the September quarter, after a revised 2.2% gain in the June quarter.

- Wednesday – US – Gross Domestic Product grew at an annual rate of 2.1% in the September quarter.

- Thursday – AUS – Private Capital Expenditure

Australian Market

The Australian sharemarket edged 0.2% lower on Wednesday, as price movements were largely attributable to commodity related stocks. The Energy sector continued to steam ahead, up 1.2%, after crude oil prices responded positively to lower than expected US strategic petroleum reserves. Furthermore, the expectation that OPEC will move to tighten oil supply, amid the release of global reserves, also buoyed prices. Major movers in the sector included Woodside Petroleum (1.6%), Santos (2.3%) and Beach Energy (2.4%).

Meanwhile, iron ore miners rallied as the commodity price rose ~4.4% to just below US$100 a tonne. The uplift in price can be attributed to rising profit margins for steel producers and signs that Chinese authorities might implement expansive monetary and fiscal policy. Index heavyweights BHP and Fortescue rose 0.5% and 1.3% respectively, while Rio Tinto closed flat.

The Financials sector closed in the red, down 0.3%, after a mixed performance by the major banks. Commonwealth Bank (0.4%) and ANZ (0.9%) closed higher, while Westpac and NAB both edged 0.1% lower. Uncertainty around interest rates and reported tight net interest margins continued to dampen the sector. Fund managers were also mixed, as Australian Ethical Investment rose 1.0%, while Macquarie Group (-1.5%) lost momentum.

The Australian futures point to a flat open today.

Overseas Markets

European sharemarkets ended a four day losing streak on Wednesday, however, concerns around the region’s worsening COVID-19 situation, and the prospect of lockdowns, restrained the market. This, coupled with price pressures and likely interest rate hikes, has dampened Europe’s economic growth outlook. Travel stocks fell by over 1.0%, to extend losses for a seventh straight day. Notable gainers included HelloFresh (0.8%) and water utilities provider United Utilities Group (1.3%). By the close of trade, the German DAX lost 0.4%, while the UK FTSE 100 gained 0.3% and the STOXX Europe 600 edged 0.1% higher.

US sharemarkets firmed on Wednesday, following better than expected consumer spending growth in October (1.3%), which propped up the economy as it equates to ~70% of GDP. The Consumer Discretionary sector closed 0.2% higher, despite shares in retailers like Gap (-24.1%) and Nordstrom (-29.0%) plummeting due to supply chain issues. The Real Estate (1.3%), Energy (1.0%) and Information Technology (0.8%) sectors were the strongest performers. Notable gainers included online payment providers Shopify (3.5%), Visa (2.4%) and PagSeguro Digital (3.4%). By the close of trade, the S&P 500 rose 0.2%, the NASDAQ lifted 0.4% and the Dow Jones closed relatively flat.

CNIS Perspective

Further evidence of Australia’s resilience during the most recent lockdowns was found in yesterday’s construction data.

Lockdowns and restrictions on travel has encouraged more home renovation and the construction sector is being supported by a robust pipeline of work in the home building space and policy incentives such as the HomeBuilder program.

Private sector residential building work rose by 0.1%, driven by an increase in new private sector house construction of 3.3%. New private sector house construction was 17.2% above pre-pandemic levels.

Additionally, governments have committed to increased spending on infrastructure projects as part of the fiscal policy response to the pandemic.

Should you wish to discuss this or any other investment related matter, please contact your Investment Services Team on (02) 4928 8500.

Disclaimer

The material contained in this publication is the nature of the general comment only, and neither purports, nor is intended to be advice on any particular matter. Persons should not act nor rely upon any information contained in or implied by this publication without seeking appropriate professional advice which relates specifically to his/her particular circumstances. Cutcher & Neale Investment Services Pty Limited expressly disclaim all and any liability to any person, whether a client of Cutcher & Neale Investment Services Pty Limited or not, who acts or fails to act as a consequence of reliance upon the whole or any part of this publication.

Cutcher & Neale Investment Services Pty Limited ABN 38 107 536 783 is a Corporate Authorised Representative of Cutcher & Neale Financial Services Pty Ltd ABN 22 160 682 879 AFSL 433814.