Pre-Open Data

Key Data for the Week

Key economic data released this week:

- Tuesday – AUS – RBA Interest Rate Decision – the RBA decided to leave the cash rate on hold at 0.25%.

- Tuesday – US – Trade Balance deficit widened from US$63.4 billion in July to US$67.1 billion in August.

- Wednesday – EUR – ECB President Lagarde Speech

- Wednesday – US – FOMC Minutes

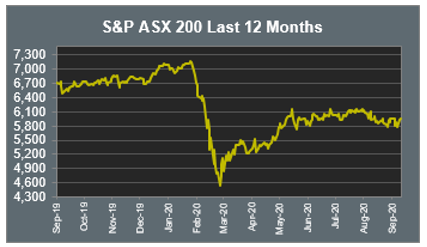

Australian Market

The Australian sharemarket closed higher yesterday, up 0.35% in a mixed session of trade, as investors awaited last night’s Federal Government Budget announcements.

Materials outperformed yesterday, with the mining heavyweights closing higher; Fortescue Metals added 1.7%, while BHP and Rio Tinto gained 0.4% and 0.3% respectively. Goldminers, Saracen Mineral and Northern Star, were the top performers on the market, up 9.6% and 10.6% respectively, after the companies agreed to a $16 billion merger. The merger will make the company the second largest Australian gold miner and a top 10 global producer of gold.

Energy also led the market; Santos gained 3.5% and Oil Search rose 3.0%, while Woodside Petroleum and Ampol added 2.2% and 2.0% respectively.

The Health Care sector was the worst performer on Tuesday, down 0.8%. Ramsey Health Care lost 1.8%, Cochlear slipped 1.5% and CSL fell 0.8%, while Sonic Healthcare bucked the trend, up 0.2%.

The Australian futures market points to a 0.29% fall today.

Overseas Markets

European sharemarkets closed higher overnight with gains extending into a fourth consecutive session. The Financials sector outperformed as banks rose 3.0% amid hopes of a US stimulus package, a Brexit trade deal, and positive German economic data. Deutsche Bank added 5.7% and Barclays gained 4.8%, while Lloyds Bank rose 3.6%. The German DAX rose 0.6%, while the broad based STOXX Europe 600 and UK FTSE 100 both added 0.1%.

US sharemarkets closed weaker on Tuesday as US President Trump announced he has rejected the Democrats’ US$2.4 trillion proposal for a fifth COVID-19 stimulus. All sectors closed in the red except for Utilities, which gained 0.9%. The Consumer Discretionary sector was the weakest performer, down 2.1%. eBay slumped 4.0% and Amazon fell 3.1%, while Starbucks lost 1.7%. Information Technology also underperformed; Apple slumped 2.9% and Facebook lost 2.3%, while Alphabet and Microsoft slipped 2.2% and 2.1% respectively. By the close of trade, the NASDAQ fell 1.6%, the S&P 500 lost 1.4% and the Dow Jones slipped 1.3%.

CNIS Perspective

Last night, Josh Frydenberg flagged net debt of ~$703 billion, which is set to rise with further deficits in coming years to ~$966 billion by 2023-24. Scary figures for a country that has had a strong history of economic management.

However, if you are going to be racking up debt, now is the time. While the deficit and the accompanying debt will reach records, our saving grace is interest rates at historical lows.

The government can now borrow money for 10 years at the miserly rate of around 0.85%.

Such low rates make debt servicing far easier than ever before. As debt built up in the 1990s after Australia’s previous recession, debt servicing as a proportion of government revenue reached 7.1%.

While the debt figures might be hard to comprehend, debt interest payments are more important, and expected to reach just 2.9% of government revenue in 2020-21, a very manageable position to be in, and a far cry for the exit of Australia’s previous recession.

Should you wish to discuss this or any other investment related matter, please contact your Investment Services Team on (02) 4928 8500.

Disclaimer

The material contained in this publication is the nature of the general comment only, and neither purports, nor is intended to be advice on any particular matter. Persons should not act nor rely upon any information contained in or implied by this publication without seeking appropriate professional advice which relates specifically to his/her particular circumstances. Cutcher & Neale Investment Services Pty Limited expressly disclaim all and any liability to any person, whether a client of Cutcher & Neale Investment Services Pty Limited or not, who acts or fails to act as a consequence of reliance upon the whole or any part of this publication.

Cutcher & Neale Investment Services Pty Limited ABN 38 107 536 783 is a Corporate Authorised Representative of Cutcher & Neale Financial Services Pty Ltd ABN 22 160 682 879 AFSL 433814.