Snapshot

Global financial markets experienced a textbook September, trading lower during the month in response to higher oil prices and higher bond yields.

Market volatility, as measured by the CBOE Volatility or VIX index, rose to 17 after starting the month around 13.

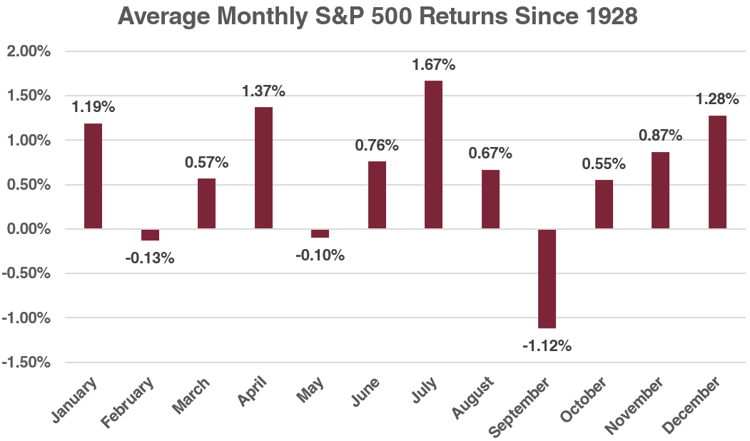

Historically, the month of September is known for its weak stock market returns, a phenomenon often referred to as the "September Effect". Since 1928, the S&P 500 index has, on average, fallen by 1.12% during this month. However, it is worth noting that despite September's historical downturns, the subsequent months of October, November, and December have typically witnessed stronger returns, with increases of 0.55%, 0.87%, and 1.28% respectively.

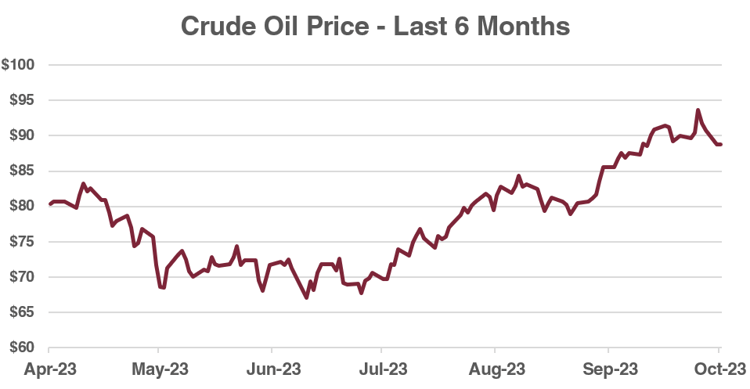

The commodities market also saw shifts in September. While most commodities experienced a decline, oil and iron ore stood out with increases of 2.4% and 1.1% respectively.

The surge in oil prices over the past three months, amounting to a 21% increase, can be attributed to significant production cuts from Saudi Arabia and Russia. These nations voluntarily reduced their oil production by 1.5 million barrels a day in July to counteract declining fossil fuel demand and support prices.

Though this reduction was initially intended as a short-term measure, it has been extended to last until the end of 2023. Additionally, these voluntary cuts came on top of the production reductions agreed upon by OPEC+ in June.

There are potential risks associated with these market dynamics. If oil prices remain higher for longer, they will contribute to more persistent inflation and counteract restrictive monetary policy from central banks.

Elevated oil prices keep pressure on household budgets, both directly via petrol and indirectly through other goods and services, as increased costs of goods lead companies to raise prices and maintain profit margins.

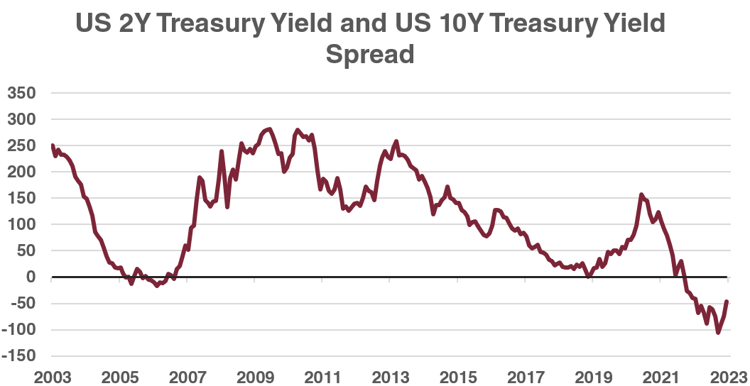

Bond yields rose accordingly, with the yield on the 2-year US Treasury rising by 0.22% to 5.11%, and the yield on the 10-year US Treasury rising by 0.49% to 4.68%. Interestingly, the US yield curve also remains inverted, signalling slower economic growth ahead, with the 10-year US Treasury yield of 4.68% trading below that of the 2-year US Treasury yield of 5.11%.

As we move forward, it remains to be seen whether market movements in September are the beginning of a new trend, or if the coming months will revert to their usual seasonal patterns. If the seasonal narrative holds up, the fourth quarter can often lead to a “Santa Claus” rally and strong equity market returns.

Key Stocks

Wade is the head of the Investment Services division at Cutcher & Neale and has over 15 years of industry experience in accounting and investment advisory roles.

Wade guides his division on the belief that investment portfolios should be built on transparency and flexibility. His expertise focuses on direct portfolio exposure to both Australian and Global Investment markets.

.jpg?width=352&name=Investment%20SnapShot%20Header%20-%20March%202024%20(1).jpg)